ACH Payments. A Brief Introduction

ACH is an efficient payment option that has become one of the safest and largest systems in global finance. Every year, ACH transactions are estimated to total $43 trillion. This quick and cost-effective way of transactions has become attractive to many businesses.

Most business owners have heard of ACH payments, but might not be sure how it works. This article explains the basics of ACH and how it is different from other payment modes.

Table of contents

ACH Definition

Let’s give a definition – what is an ACH payment? Automated Clearing House (or ACH) is a network that is employed in electronic bank transactions known as ACH payments. ACH transactions involve two computers, one for sending a request for payment, and another to accept the request. The ACH network is used in both computers to communicate with each other in order to send and receive payments.

The ACH payment method is used in the US to pay bills, loans, mortgages, and wages and make direct deposits. There are few rules established by the National Automated Clearing House Association or NACHA. Those rules or guidelines should be maintained while making electronic payments through an ACH network.

Various Types of ACH Transactions

Two types of ACH transactions are available, which include direct payment and direct deposit.

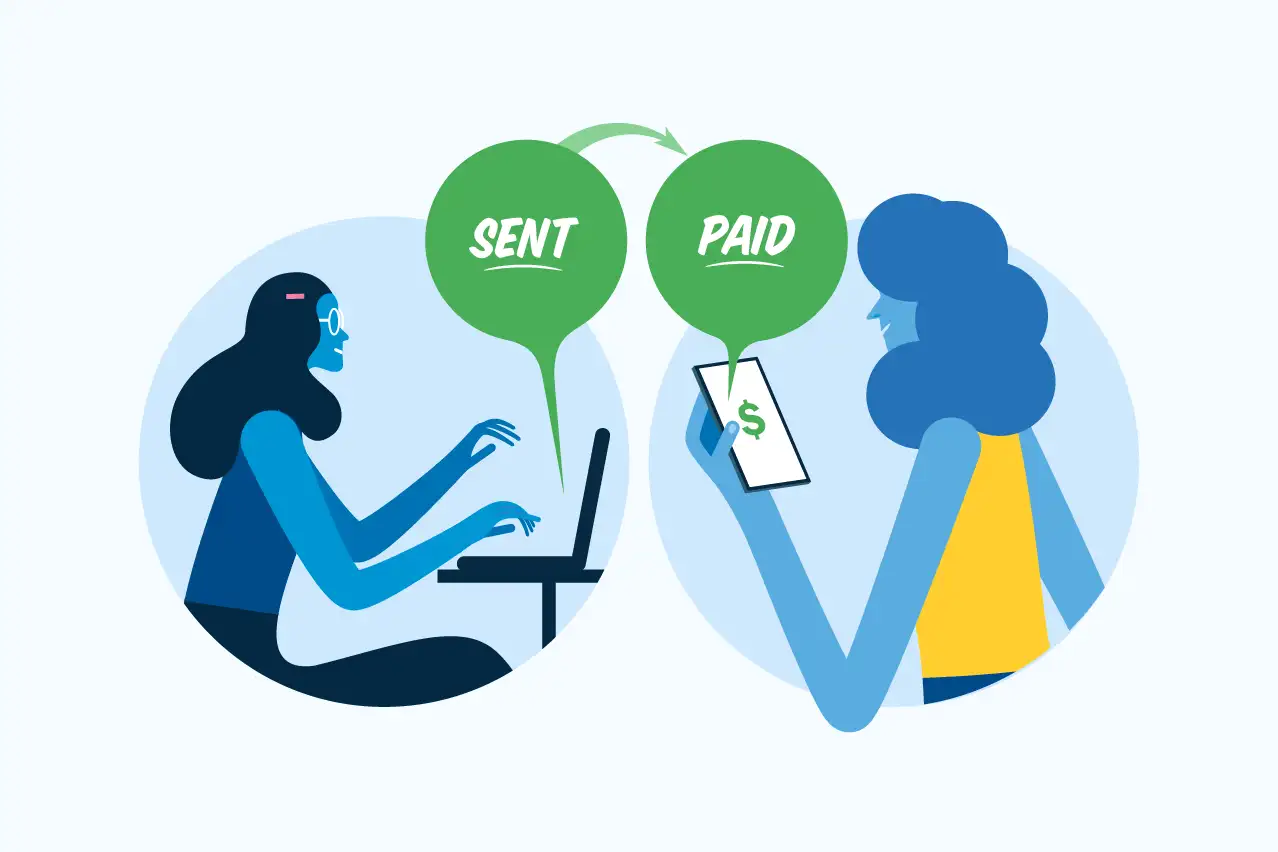

Direct payments: The recipients usually initiate direct payment to request funds- for example, to collect payment for recurring bills automatically.

Direct deposits: Payers use this method to make payments directly to a receiving account- for example, to pay wages to the employees.

The Way ACH Payment Work

ACH transactions involve a data file that contains required information about the chosen payment. When you process the transaction, you need to send that file to the originator’s bank, to the clearinghouse, and to the recipient’s bank respectively. The funds will then be removed from the receiving account.

Here is the entire procedure of ACH direct payment. Look at it prior to initiate the payment.

Required Setup

Prior to making the transaction, you need to make sure that the bank account of your customer allows you to pull money. If your customer is willing to give you permission, he or she can fill the authorization form in the bank.

Initiation

You can start the procedure by sending data files to your ODFI, or Originating Depository Financial Institution. Every detail about the bank accounts, routing numbers, and transaction type are included in the file.

Batching

The ODFI collects the transaction data files and forwards them to an ACH operator. The operator is either FedACH (the Federal Reserve Banks’ Automated Clearing House) or EPN (the Electronic Payments Network).

Distribution

Then, the ACH operator sends the data files to the bank of your customer, known as Receiving Depository Financial Institution (RDFI).

The Final Step

The RDFI pulls the required amount from the account of your customer. You will get notified when the transaction is done, and you receive the payment.

A Comparison Between ACH Payments and Others

The ACH payment procedure is much more efficient than other alternatives, such as credit or debit cards, check, wire transfers,s or cash payments. It offers better security, lower transaction costs, and more convenience.

Cost-effective

ACH payment contains a lower transaction cost when compared to others like credit cards and wire payments. Transaction costs include in credit cards is 2% of the total payment amount and in a wire transaction, it is $10-35. However, ACH transactions cost less than $1.

Reversible

Wire transfers are quick but irreversible. In addition, it does not offer any way to verify the identity of the sender or recipient. On the other hand, payments are reversible in ACH and the identity of the users can be authenticated.

Secure

Concern about security comes with every mode of a financial transaction. Payment errors may occur with bounced checks, wire transfers sent to the wrong recipient, and misused information of credit cards. ACH allows secure payment by allowing direct transactions between the sender and the receiver without using any mediator.

Repeatable

ACH transaction goes well with recurring payments. The reasons include-

- Recurring payment with ACH transactions provides you with the convenience of spending less time on each transaction.

- The system is automated. Therefore, your customer does not have to worry about missing payments.

- You can get the payment at the right time.

Better for Retention

Payment failure is another problem associated with other procedures. ACH has lower failure rates compared to credit card payments, as the payment is made directly from account to account.

Conclusion

Utilizing an ACH network simplifies the means of payment for the business owners. It is an economical and secure way of transferring money from one account to another. The simplicity and retention ability have made it popular in business transactions, especially if recurring payment is required. In this modern era, where an electronic transaction is essential for every business, switching to ACH is simply a smart move.